Renewable energies, digitalisation and e-mobility – as soon as these terms are heard on the stock market, the majority of investors will initially think primarily of manufacturers of wind turbines, providers of streaming services and makers of electric cars. These 3 mega trends have an Achilles heel, though, in the form of rare earths. This type of metal is used in countless technological applications, ranging from batteries through smartphones to the electric motor. Contrary to what the name might suggest, these raw materials are not that rare today. This could change, however, as soon as the current growth forecasts become reality. To use e-mobility as an example, 1.1 million vehicles driven by electricity or renewable energy were estimated to have been delivered in 2017. By 2030 this market could have grown to 30 million units.

In the view of the investment experts of Swissquote, demand for metals of the rare earths is set to increase by 15% in the next few years. The shortage of these raw materials that this forecast suggests has led the online broker to launch the Swissquote Rare Earth Index. The new benchmark targets companies that are in the best position to profit from the increasing demand and shortage. Their business strategy is focused on the rare earths and they generate the majority of their sales in this sector. On the value chain the index sponsor looks at the exploration, mining and processing stages. To come into consideration for the dynamic yardstick, a share must also meet quantitative requirements. In addition to a market capitalisation of at least USD 100 million, these include an average daily trading volume of around USD 100,000. The sponsor rebalances the index every three months. In certain cases, such as new listings, an extraordinary adjustment is also possible.

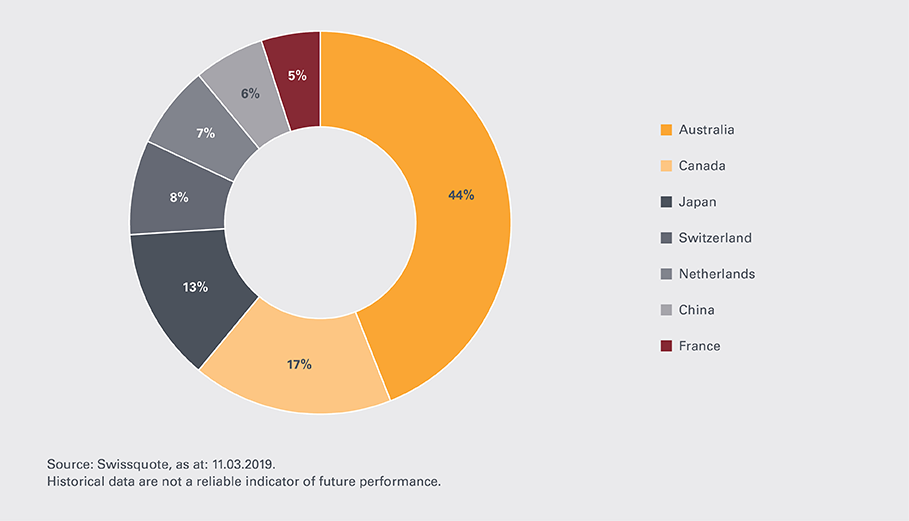

The managers can include up to 20 members in the Swissquote Rare Earth Index. The initial composition consists of 15 companies from 7 different countries. Australian companies lead the way with a weighting of 44% in total (see graph). They include Iluka Resources. The Perth-based specialist in the mining of mineral sand regards itself as the world’s biggest producer of natural titanium dioxide. This raw material is used in pigments (dyes), titanium metal and welding technology. Iluka is also the global leader in the extraction of zircon. The opacity of this metal and its resistance to heat, water, chemicals and abrasion make it high in demand. The mining group presented its accounts for 2018 at the beginning of March, reporting a scarcity of zircon in key markets. Together with the price increases that have been implemented, this factor led the group to record a 22% growth in sales. It also saw Iluka Resources effect a turnaround after 2 years in the red.

Management fee: 0.70%

Index Sponsor: Swissquote Bank SA

Issuer: Leonteq Securities AG

By contrast, last year Glencore suffered a 41% collapse in net profits to USD 3.4 billion. Write-downs were the primary cause of this development. On the operational side, the British-Swiss mining group profited from higher raw materials prices. Glencore posted an 8% rise in its adjusted EBITDA to USD 15.8 billion. Group boss Ivan Glasenberg announced a new share buyback programme amounting to USD 2 billion. Two global mega trends make the CEO optimistic: “Our commodity portfolio and its key role in enabling the energy and mobility transition for a low-carbon economy enables us to look ahead with confidence.” To a certain extent Glasenberg is speaking for the whole sector. Investors who share this assessment have recently had the opportunity to diversify their investment into rare earths.

We look forward to answering all of your questions about our products and how they are traded. Please don't hesitate to get in touch! Phone: 058 800 11 11, email info@leonteq.com or contact us here.