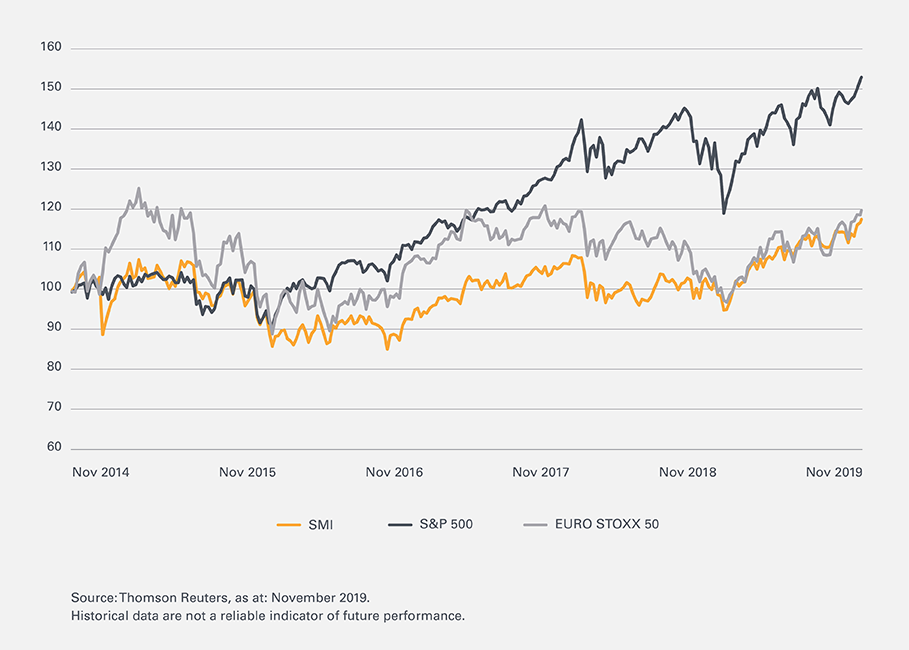

Following a truly golden October, the weather turned at the start of November, autumn introducing itself with fog, wind and rain. There is still no sign of any gloom on the stock market, though: both the Swiss equity market and Wall Street reached new peaks after the turn of the month. That means stock markets are heading into the final straight of the year with plenty of momentum. Eight weeks before New Year, the interim 2019 balance sheet for SMI®, S&P 500® and EURO STOXX® 50 shows gains of more than one fifth for each (see graph). One of the key drivers of the rally is monetary policy, with the main central banks having pursued a very expansive course for years. They have to all intents and purposes done away with the safe interest rate. To take the example of Switzerland, in summer the yield on 10-year Swiss treasury stock fell below the -1.00% mark. While the interest on this benchmark bond has recently increased somewhat, it remains stubbornly in the red.

Negative interest rates are now also being felt by well-off savers, with a number of Swiss banks passing on to their customers the burden resulting from the central bank's policy. They are deducting the negative interest when cash holdings in Swiss francs reach a certain level. However, those affected do not have to simply take this hit on the chin: the market for structured products offers opportunities to generate ongoing income while at the same time circumventing the stock market risk to a certain extent. True to the motto "Negative interest rates? Not with us!", Leonteq has come up with an interesting new issue. The independent expert for savings and investment solutions is bringing together the three stock market barometers already mentioned. The SMI®, EURO STOXX® 50 and S&P 500® will ensure a broadly diversified basis for the Callable Multi Barrier Reverse Convertibles. Underlying the products are 570 large caps from Switzerland, the eurozone and the USA.

Leonteq is offering the product in two different currencies. For the CHF and EUR tranche, the issuer is guaranteeing an annual coupon. For both variants the barrier is set at an predefined level of the initial fixing. This mark will only be put to the test on the maturity date, when the SMI®, EURO STOXX® 50 and S&P 500® will all have to be running higher than the protection threshold. Given the European barrier, the course of the benchmark up to the review date is irrelevant. As long as no index falls at or below the barrier at Final Fixing Date, investors will get their nominal back in full. In this case the investment will end with the maximum return.

To trigger a breach of a barrier, the SMI®, for example, would have to fall back to a level last seen in September 2011. Of course, there is no such thing as absolute certainty on the stock market: should the cushion not be sufficient for at least one underlying market, the partial protection would lapse. In this case the repayment would be linked to the index with the worst performance. Investors would thus have to reckon on significant discounts. It is possible that the Barrier Reverse Convertibles will not even reach the final maturity date, as Leonteq has a right of termination. The issuer can make use of the callable option every 12 months. In the event of termination, investors would receive the pro rata coupon in advance alongside the full nominal. This design feature brings with it the risk associated with reinvestment. The possible expense is covered by the product terms offered. To conclude, the new issue outlined is a comparatively conservative structure. The mood on the stock market would have to turn extremely sour for investors to "miss" this way out of the interest rate valley.

We look forward to answering all of your questions about our products and how they are traded. Please don't hesitate to get in touch! Phone: 058 800 11 11, email info@leonteq.com or contact us here.