Exchange Traded Products (ETPs) provide access to a wide range of asset classes. In addition to entire equity markets, sectors, and regions, commodities, cryptocurrencies, and currencies are also part of the spectrum covered by these passive financial instruments. Structurally, an ETP represents a claim in the form of a securitised note. To mitigate issuer risk, ETPs are collateralised through the pledge of assets (collateral portfolio). These assets may consist of securities, precious metals, or cash. The flexible application possibilities, combined with liquid and transparent exchange trading, have led to a steadily growing product universe. While the segment was initially dominated by commodities, cryptocurrencies have now become the main growth driver – with many ETPs tracking a digital currency such as Bitcoin.

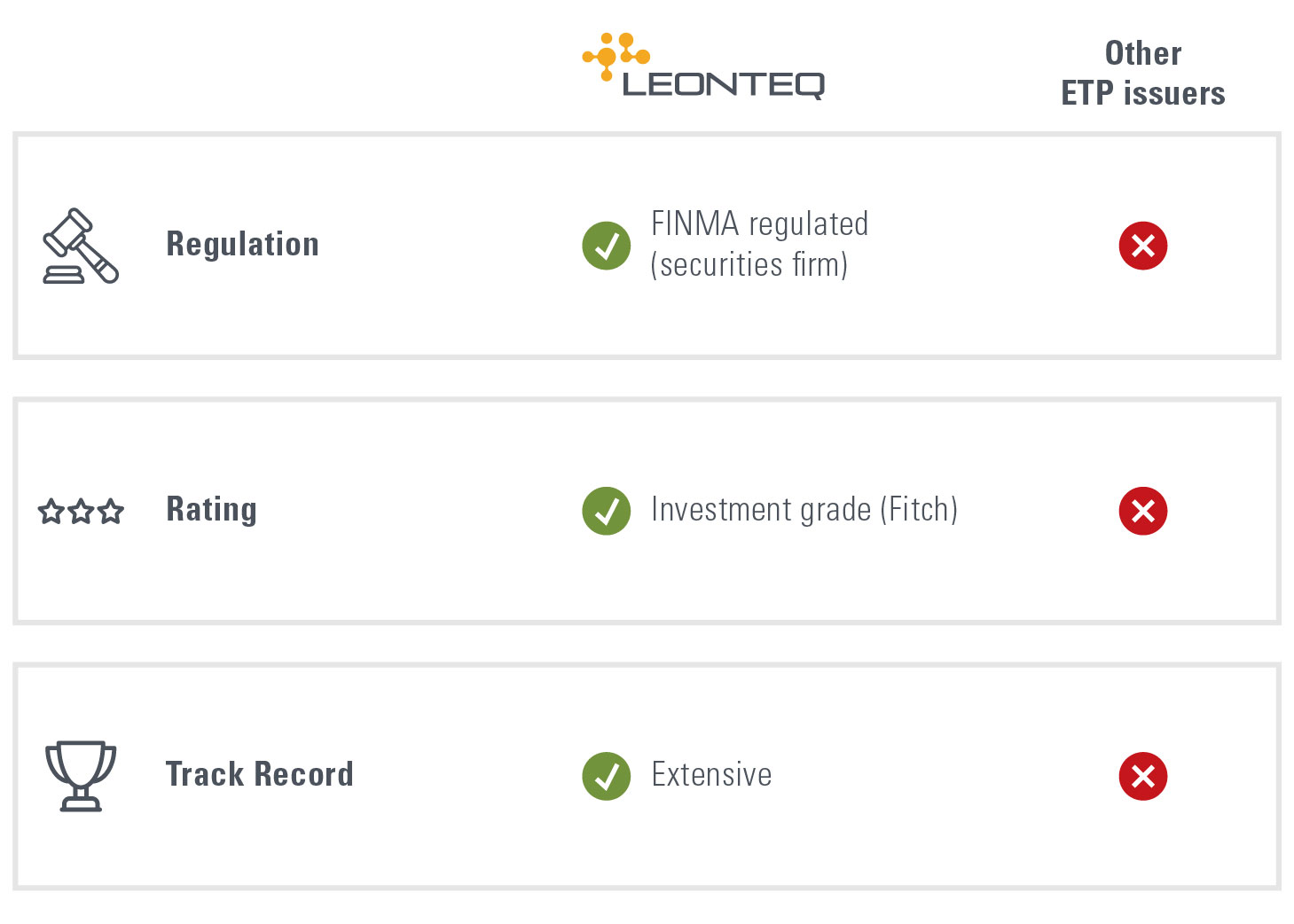

Leonteq is now taking steps to further develop this market both structurally and in terms of the range of underlying assets. The Zurich-based fintech company has introduced the ETP+ label. At the core of this innovation lies enhanced investor protection. To date, many ETP issuers have been special purpose vehicles without ratings or regulatory supervision, often operating with only minimal financial resources. Leonteq, on the other hand, brings a 15-year track record as a successful issuer of structured investment products. As the first ETP provider in Switzerland, the company is licensed and supervised by FINMA as a securities firm and holds an investment-grade rating from Fitch.

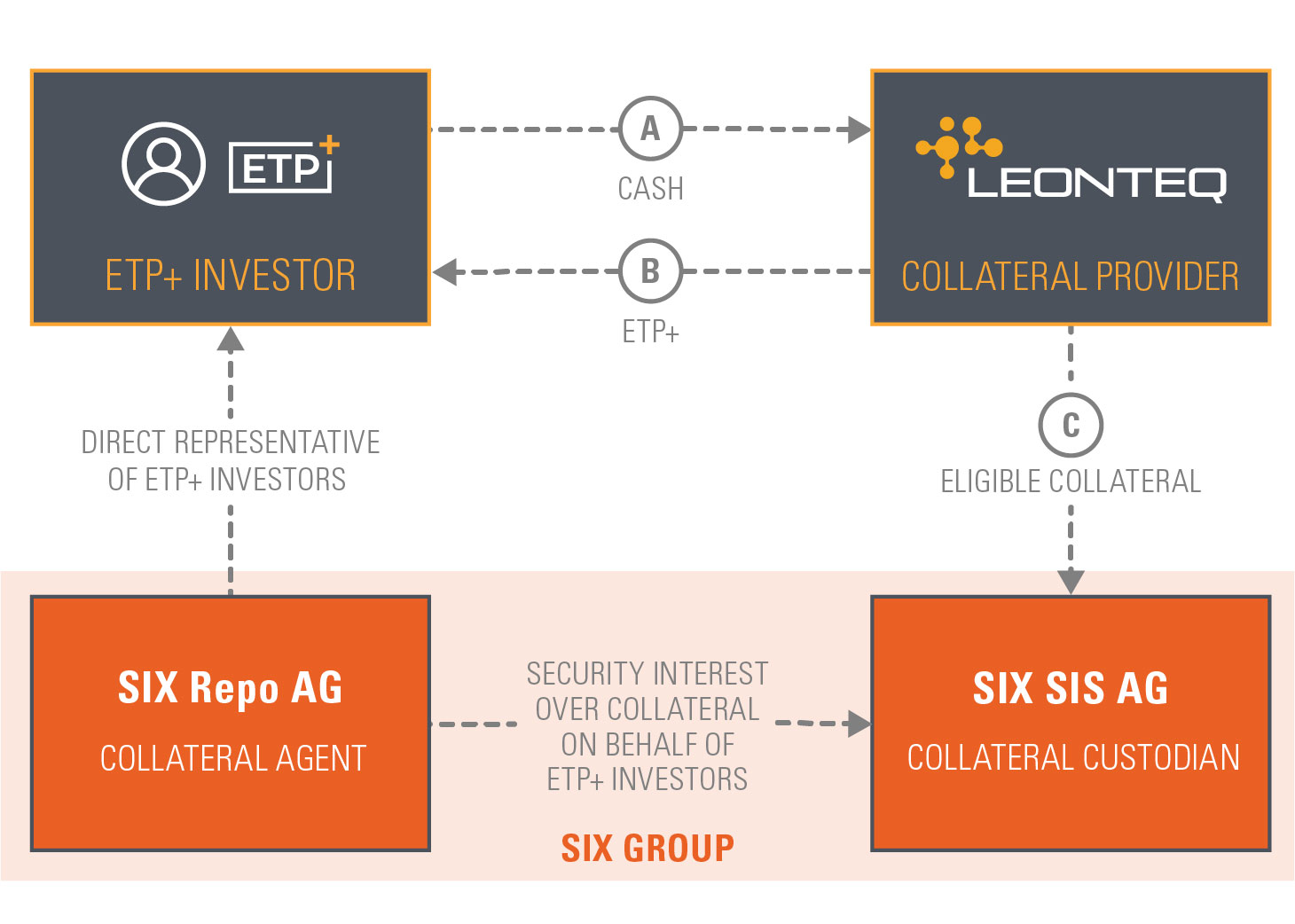

Another key advantage of ETP+ lies in its collateralisation structure. In cooperation with the SIX Group, Switzerland’s central financial infrastructure provider, Leonteq Securities AG has implemented a robust collateral framework for ETP+. Under this model, the collateral assets are held with SIX SIS AG (the collateral custodian) and are subject to independent and intraday monitoring by SIX SIS AG to ensure that all positions remain fully collateralised at all times.

Leonteq Securities AG has no disposal rights over the assets held in the collateral account and cannot dissolve or transfer this account. SIX Repo AG acts as collateral trustee and as the direct representative of ETP+ investors.

In the event of certain predefined circumstances – such as under-collateralisation, payment default, or insolvency of Leonteq Securities AG – SIX Repo AG will realise the collateral in the best interest of investors. The objective of this collateral model is to significantly reduce issuer risk.

We look forward to answering all of your questions about our products and how they are traded. Please don't hesitate to get in touch! Phone: 058 800 11 11, email info@leonteq.com or contact us here.